From NASFAA:

“The City Colleges must scrap its fee-laden debit card program for student loans because the fees are illegal, the U.S. Department of Education said in a recent letter to the district,” Chi Town Daily News reports. “In a July 7 letter, the agency wrote that students can’t be charged fees for using an ATM or visiting a teller to get their money … The letter comes two months after the agency first said the existing program was fine. Stephanie Babyak, a spokeswoman at the Education Department, said it reversed its own decision after asking the City Colleges some more questions about the debit card program. While the program was running, the first withdrawal from an ATM or a teller was free but future visits to an ATM cost $2 and talking to a teller cost $10. In May, the Department of Education told the City Colleges the program was acceptable since students had other ways of getting their refund money. They could wait for paper checks or get the funds direct-deposited into a bank account, the agency noted … Though the City Colleges does not face any sanctions for running the debit card program as it did, the Department of Education said it wants a response from the district about how it will fix the program.”

Commentary

With luck, the trend will spread of eliminating fees of any kind on debit cards for tuition rebates and student financial aid disbursements. These fees line the pockets of banks and schools with no measurable benefit to students other than not having to cash a physical check. Moreover, the disbursements themselves are usually the proceeds of a student loan, which means that students are paying additional fees on borrowed money, in effect paying twice for money that they’re already paying money on.

News You Can Use

One of the most insidious ways you can lose money, a little bit each day, is to do business with a major commercial bank that nickels and dimes you to death with fees. Everything ranging from fees for checking accounts to ATMs to Internet home banking to overdraft fees can add up to hundreds of dollars a month if you’re not careful.

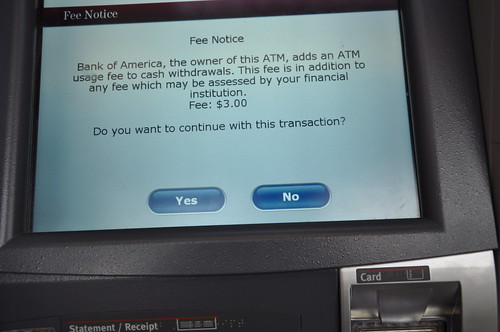

Here’s an example – I recently went to withdraw money at a local ATM:

I walked away after seeing a $3 fee, knowing that the local convenience store ATM fee, just a few doors down, was $1.75.

There are three concrete steps you can take to protect your own wallet and deliver a strong message to commercial banks:

1. Don’t bank with a commercial bank. Look at community banks and especially credit unions for banking services that rival or exceed what commercial banks can deliver (often with much better service!) and no fees or very few fees. I’ve been a customer of a federal credit union for almost a decade and can happily say that my credit union (where the staff greets me by name) has no fees on 95% of its services. The SUM network of ATMs means no fees any time I use a SUM ATM, so I save money there. No fees for Internet home banking or Internet bill pay. I used to pay probably about $100/year in fees after all was said and done when I banked with a commercial bank long ago. Since then, banking with a credit union has saved me all those fees – over the span of a decade, $1,200. Who wouldn’t want $1,200 more free money?

2. Don’t patronize commercial bank ATMs. Every time you pay their inflated fees, you implicitly endorse their business practices and give them every reason to continue or increase their ATM fees. Go Google for ATM locators and find ATMs nearby that offer low fees or no fees. Join a credit union that’s a member of the SUM network and look for no-fee ATMs around you.

3. If you need to withdraw a small amount of cash – under $100 – and there no no-fee option around, go to any supermarket that offers cash back at the register and buy a pack of gum or some other consumable. You’ll pay about the same amount as an ATM fee but you’ll have something to show for it.

Finding a credit union is easy. Go to the National Credit Union Administration (NCUA) and use their search tool to locate a credit union near you. The NCUA is identical to the FDIC in terms of guarantees on your savings, so any money you have with an NCUA insured account has identical safety and coverage to FDIC insured bank accounts.

Additionally, many colleges have credit unions right on campus. Usually they’re set up primarily for employees of the college, but many allow students to bank with them as well. A commercial bank will almost always have an ATM on campus in a prominent place with high fees to sucker unaware students, but campuses with credit unions on campus almost always have a no-fee ATM as well. Save yourself some money and find it on your campus if you have one.

No comments:

Post a Comment